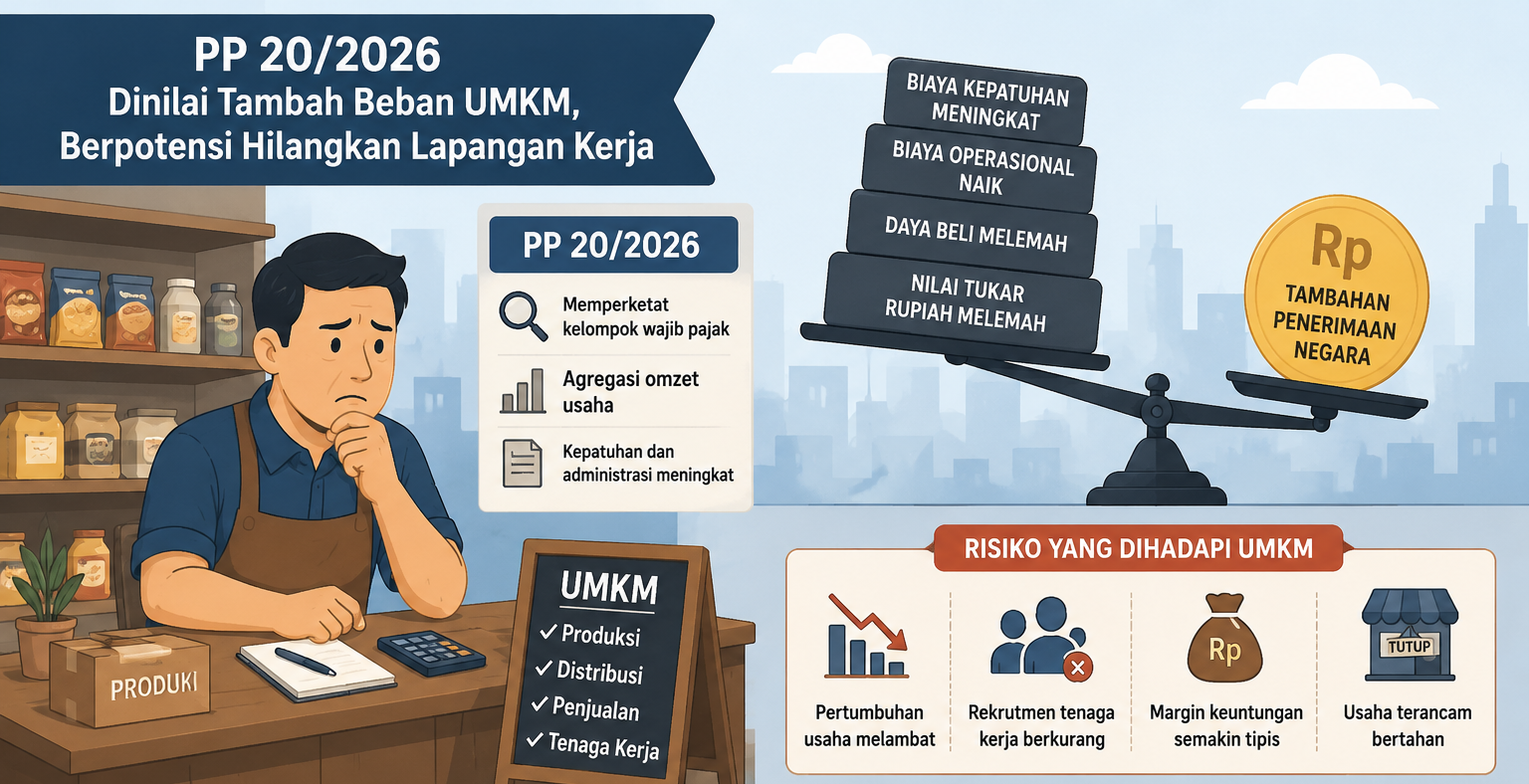

Govt Regulation 20/2026 Deemed to Add Burden on MSMEs, Potentially Eliminate Jobs

The FINE Institute has warned that the implementation of Government Regulation (PP) No. 20/2026 needs to be carefully scrutinised as it could potentially generate greater economic costs than the expected additional state revenue. The government is indeed maintaining the Final Income Tax (PPh) rate for MSMEs at 0.5 percent. However, through PP 20/2026, the government has tightened the criteria for taxpayer groups eligible for this facility and introduced a turnover aggregation mechanism to prevent business-splitting practices.

According to Kusfiardi, Political Economy Analyst and Co-Founder of the FINE Institute, the government’s aim to improve tax compliance and close loopholes for tax avoidance is commendable. However, the effectiveness of the policy needs to be viewed more broadly, not only from the perspective of state revenue but also its impact on business continuity, investment, and job creation.

“The main issue is not the 0.5 percent tax rate because that rate has not changed. What has changed is who is entitled to that facility. The question is whether the business groups that lose this facility actually have a sufficiently large economic capacity to provide significant additional state revenue?” Kusfiardi stated on Wednesday (3/6/2026).

Kusfiardi reminded that the implementation of PP 20/2026 comes at a time when some MSME players are still facing considerable pressure. The slowdown in public purchasing power, rising production costs in several business sectors, increased logistics costs, and global economic uncertainty have narrowed the profit margins for many business actors.

Under these conditions, any policy change that potentially increases compliance costs needs to consider the real ability of MSMEs to adapt without sacrificing their business continuity. The FINE Institute also noted that the weakening of the rupiah exchange rate against the US dollar recently has increased the cost of importing raw materials, capital goods, and various production components still dependent on foreign supply.

For many MSMEs, particularly in the trade, small-scale manufacturing, and processing sectors, this exchange rate pressure squeezes already relatively thin profit margins. “In such a situation, the room for business actors to absorb additional administrative or compliance costs becomes increasingly limited. Therefore, the evaluation of PP 20/2026 cannot be separated from the macroeconomic conditions currently faced by the business world,” said Kusfiardi.

According to the FINE Institute, there is a tendency to view turnover as a measure of a business actor’s economic capability, yet turnover is not synonymous with profit. As an illustration, a distribution business with an annual turnover of Rp4.8 billion and a net profit margin of around 3 percent only generates a profit of approximately Rp144 million per year, or around Rp12 million per month. This figure must still be used to maintain business operations, bear business risks, pay business obligations, and carry out business development.

“Nominally, a turnover of Rp4.8 billion looks large. However, after accounting for the costs of raw materials, logistics, labour, business premises rent, and working capital, its economic capacity is not necessarily as great as imagined,” he explained. The FINE Institute considers this condition to reflect the characteristics of the majority of Indonesian MSMEs engaged in the trade, distribution, food and beverage, simple services, and home industries sectors, which generally have thin profit margins but absorb a lot of labour.

The FINE Institute believes the government needs to transparently convey the estimated additional state revenue expected from the implementation of PP 20/2026. This transparency is crucial so that the public can assess whether the fiscal benefits obtained are truly comparable to the additional compliance costs borne by business actors.

“We must not let this policy generate relatively limited additional revenue while simultaneously creating greater pressure on the growth of small businesses still in the phase of capital strengthening and business expansion,” Kusfiardi stated. According to him, the measure of a policy’s success must not stop at the increase in the number of taxpayers or improved administrative compliance, but must also consider its impact on real economic activity.

The FINE Institute stressed that the group most affected is not micro-enterprises, but developing businesses with annual turnovers of around Rp5 billion to Rp15 billion. Under PP Number 7 of 2021, this group is still classified as a Small Enterprise and remains an MSME category. However, they begin to lose some of the tax facilities previously available.

This condition has the potential to create a disincentive for business actors to expand their business capacity, increase turnover, or create new jobs. Kusfiardi emphasised that the impact of tax policy does not stop at the aspect of state revenue. The majority of Indonesian MSMEs are labour-intensive businesses that serve as the source of livelihood for millions of households.

Therefore, any increase in business costs potentially affects business decisions regarding investment or hiring new workers. If compliance costs rise while business margins are relatively thin, some business actors may choose to postpone expansion, reduce labour recruitment, or hold back wage increases. “On a wider scale, this condition has the potential to affect the unemployment rate and increase the economic vulnerability of low-income households. The additional tax revenue obtained by the state must not be offset by larger social and economic costs,” he concluded.